We wish to correct a mistake we made

At the start of August, we (SunWiz) published a chart that overstated the slowdown in the Victorian residential market. This was because it inadvertently filtered out the STCs registered between the 25th-31st of July.

This chart was subsequently corrected, but not before it was picked up, modified, and published on social media. It was used to demonstrate that the Victorian installation levels had fallen well below their pre-rebate business-as-usual levels.

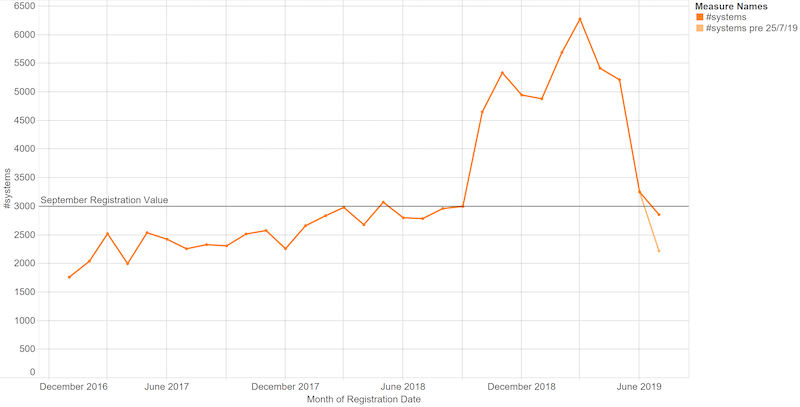

The chart below shows the difference between the initially published data, and the corrected, whole-of-month data.

This chart depicts the number of residential (sub-10kW) installations in Victoria registered in each month, based off STC registration date. It demonstrates that the number of Victorian residential systems registered in July was slightly below the pre-rebate value in September 2018.

This next chart depicts the capacity of residential (sub-10kW) installations in Victoria registered in each month, based off STC registration date. It demonstrates that the Victorian residential registration level in July was equivalent to the value in September 2018. This reflects the growing average residential system size that has occurred in Victoria since September 2018.

We wish to apologise for publishing incomplete data, and for the level of concern created by the charts containing the incomplete data.

We wish to apologise for publishing incomplete data, and for the level of concern created by the charts containing the incomplete data.

What is self-evident is the market has cooled from its peak volume, and has cooled to a level that is about the same level as prior to the introduction of the rebate. Note that due to varying lag between installation and registration, it is impossible to identify which systems registered in July:

- were supported by the rebate prior to its suspension in early 2019

- were supported by the re-opened rebate in July 2019

- proceeded without the support of the rebate

Is the market growing again?

However there are some initial signs that the market bottomed out in July and will grow in August. The next chart shows the Victorian residential capacity registered in the first eight days of each month. (We’d like to show the first 14 days of each month but the REC-Registry API is currently having issues).

The data for the first 8 days of each month shows that the start of August is towards the top-end of the pre-rebate values. Based off this data, its too soon to say how August shall pan out, but it suggests that it won’t reach the peaks seen in Q1-2019, albeit likely being higher than the volume installed prior to the introduction of the rebate.

At SunWiz we remain concerned that at the current rebate value, the quantity of rebates made available each month is far lower than demand for the rebates.

Further, as most current customers are eligible for a rebate and have been conditioned to expect a rebate, the under-supply of rebates acts as an effective cap on residential installations in Victoria.

In the short term the easiest things for the government to do would be to either increase the quantity of rebates (even if temporarily), perhaps in conjunction with a reduced rebate value.

In the medium to long term, we believe the best way to ensure the rebate settings don’t create a cap on the industry is to dynamically adjust the number of rebates and their value, based upon uptake levels.

In the meantime, commercial installations remain a major opportunity. This chart shows the (smoothed) monthly installation levels of 10-100kW systems by state. Victorian commercial installations are at record levels. However, perhaps distracted by its residential boom, Victoria has fallen behind the growth experienced in the commercial segment of NSW and QLD.

Warwick Johnston is managing director of SunWiz