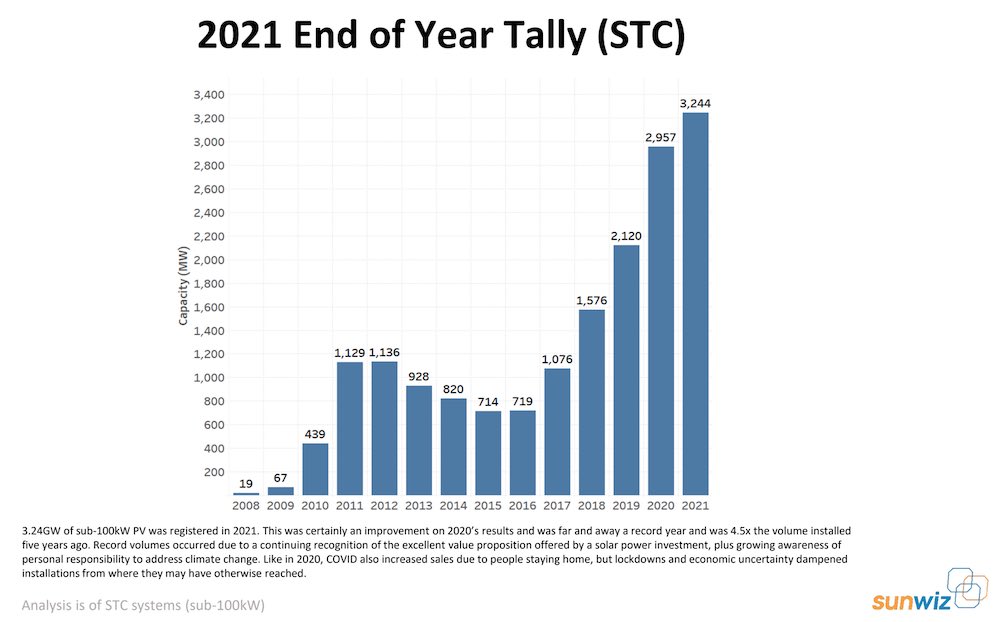

A “turbulent” 12 months for the rooftop solar industry, including Covid disruptions, supply chain chaos, regulatory ructions, and panel price rises, did not stop 2021 from winding up as another record year, with a new high of 3.24GW of sub-10kW PV capacity registered.

But a major report by leading industry analysts, SunWiz, has warned that shifting trends in the local market, coupled with ongoing global industry headwinds, could deliver the rooftop solar market’s first contraction since 2015, and break a four-year streak of record growth.

SunWiz’s newly released 2021 Australian Solar Year in Review, “The Wisdom”, looks back at a year that was “far and away a record”, delivering more than four times the volume of sub-100kW solar than was installed five years ago.

SunWiz managing director Warwick Johnston says the record volumes in 2021 demonstrate the excellent value proposition offered by solar to households and businesses, as well as a growing desire to address climate change.

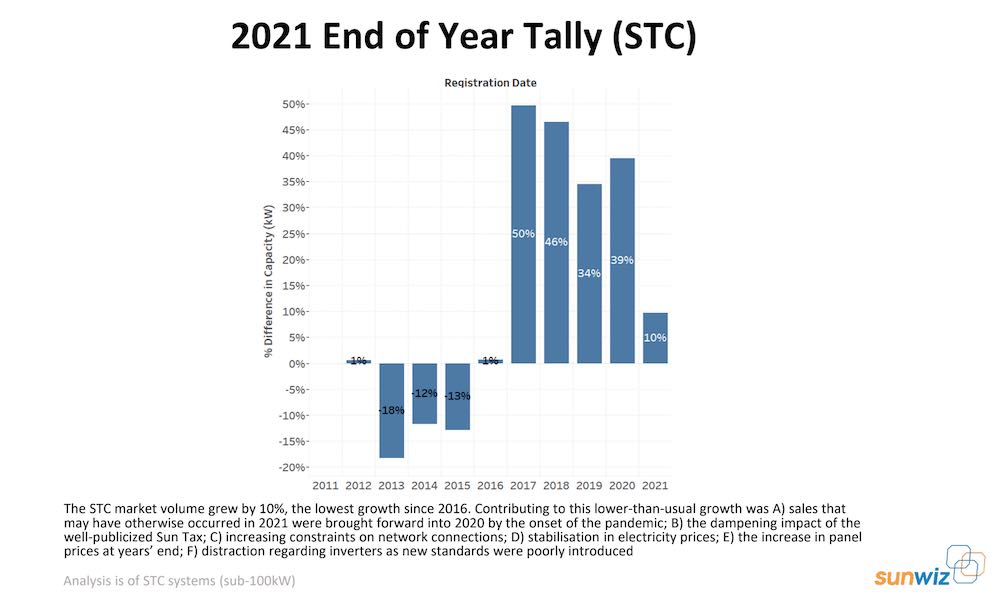

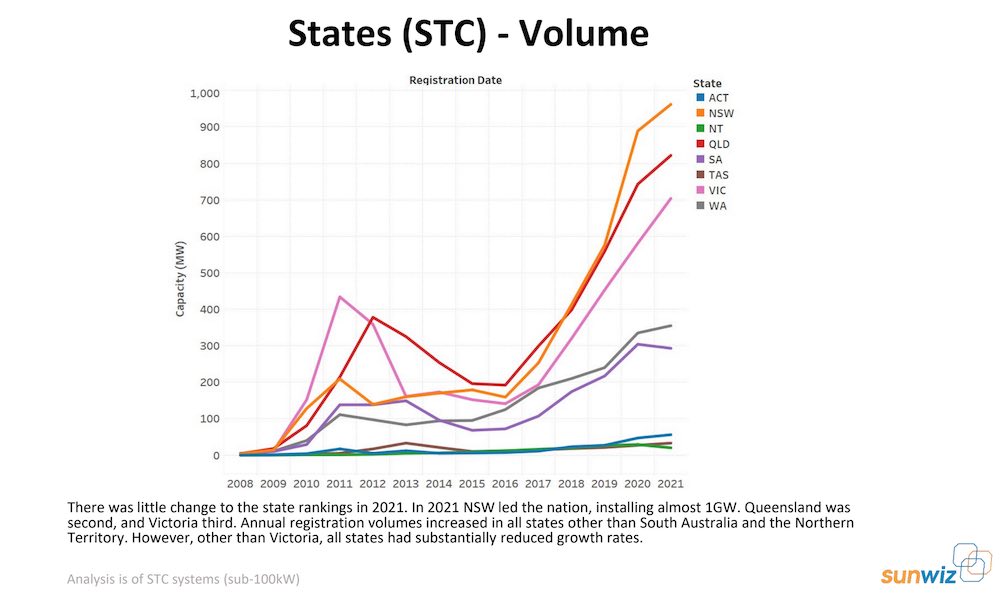

On the flip-side, SunWiz notes that the small-scale technology certificate (STC) market volume grew by just 10%, which is the lowest level of year-on-year growth since 2016, thanks to a mix of global and local issues that combined to dampen demand.

The Year in Review attributes the lower-than-usual growth in 2021 to mix of global and local issues, including the ongoing Covid-19 pandemic, changes to local regulations and network settings, and a combination of falling power prices and rising panel prices.

“Like in 2020, Covid also increased sales due to people staying home, but lockdowns and economic uncertainty dampened installations from where they may have otherwise reached,” the report says.

Another impact from Covid the report observes is that sales that may have otherwise occurred in 2021 were brought forward into 2020 by the onset of the pandemic.

On the consumer side, SunWiz says a dampening in demand might have been exacerbated by debate around the so-called “sun tax,” which refers to a charge households might have to pay in the future for exporting solar to the grid, following changes to market rules.

As One Step Off The Grid and sister site RenewEconomy have reported, the introduction of a solar export tariff has sparked strong debate, with opponents arguing it will unfairly penalise solar households and damped future demand due to its impact on the return on investment in rooftop panels.

On the other side of the argument, proponents of the rule change is the only forward for rooftop solar in light of increasing constraints on network connections that are already preventing some households from exporting to the grid at all.

And it is also argued that export tariffs could be part of a future two-way electricity pricing structure that incentivises “smarter” solar, where households are encouraged to self-consume or store solar during the day, rather than flooding the grid with PV generation when demand is low.

Other potential dampeners on rooftop solar demand noted by SunWiz were the stabilisation of electricity prices which, when combined with an increase in panel costs – driven by supply-chain shortages and bottlenecks – chip away at the value proposition of rooftop solar.

And finally, the report notes the negative impact that an end-of-year “distraction” around inverters and DC isolators, which One Step has also reported on, here and here.

“The short-notice removal of many DC isolators from the market caused momentary pain,” the report says.

“That pain grew when inverters with integrated DC isolators were prevented from certifying their product prior to the implementation of AS4777 in December 2021. An 11th–hour solution saved the day, but not before causing much angst.”

The question, now, is how these and other issues will go on to affect Australia’s rooftop solar demand in 2022. Record growth can’t go on forever, after all – and there are only so many rooftops that don’t yet have panels.

SunWiz is cautious in its outlook for 2022, noting that the end of 2021 saw some recovery in volume growth, but not to the levels seen in 2020.

“With equipment prices likely to remain high for the first half of 2022, and with significant headwinds (electricity prices and feed-in tariffs, solar remote control) the economics of PV have worsened,” the report says.

“We view market growth of 25% as very unlikely. If there is growth in the market, it’s difficult to see what the additional drivers will be other than lockdowns ceasing. Hence we believe 10% growth is the reasonable upper bound.

“It is quite possible there is market contraction, but… a downturn would be mild, say circa ~15%. Our best estimate is for a 3.15GW STC market in 2022.

But there is cause for optimism, too – or, as Johnston puts it: “there is still runway left.”

“PV still remains an excellent investment, particularly during times of economic uncertainty and low interest rates,” the report says.

“Plenty of the 3 million existing PV systems are small in size; except in recent years, the systems that were installed are insufficiently sized for today’s household requirements,” it notes, adding that larger PV system are increasingly required, particularly when you factor in future uptake of electric vehicles.

“High penetration doesn’t mean installations stopping – even in areas with high early adoption we are still trending upward,” the report says. “There is already plenty of replacement / expansion occurring.”

Ultimately, Johnston notes, regardless of volumes Australia’s is still on an upward capacity trajectory for rooftop solar – and “what reduces the financial outcome for PV improves the financial outcome for storage.” But that’s another story…

For more on this subject, listen to the latest Solar Insiders Podcast, with Giles Parkinson and Nigel Morris.

Sophie is editor of One Step Off The Grid and editor of its sister site, Renew Economy. Sophie has been writing about clean energy for more than a decade.